39 zero coupon bonds formula

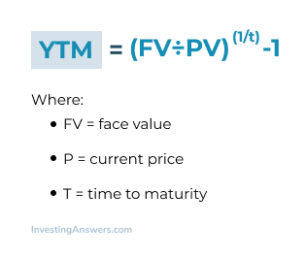

How to Calculate Yield to Maturity of a Zero-Coupon Bond - Investopedia The formula for calculating the yield to maturity on a zero-coupon bond is: \begin {aligned}&\text {Yield To Maturity}\\&\qquad=\left (\frac {\text {Face Value}} {\text {Current Bond... How to Calculate a Zero Coupon Bond Price - Double Entry Bookkeeping The zero coupon bond price is calculated as follows: n = 3 i = 7% FV = Face value of the bond = 1,000 Zero coupon bond price = FV / (1 + i) n Zero coupon bond price = 1,000 / (1 + 7%) 3 Zero coupon bond price = 816.30 (rounded to 816)

What Is a Zero-Coupon Bond? | The Motley Fool To find the current price of the bond, you'd follow the formula: Price of Zero-Coupon Bond = Face Value / (1+ interest rate) ^ time to maturity. Example 2.

Zero coupon bonds formula

Zero-coupon bond - Wikipedia A zero coupon bond (also discount bond or deep discount bond) is a bond in which the face value is repaid at the time of maturity. [1] Unlike regular bonds, it does not make periodic interest payments or have so-called coupons, hence the term zero-coupon bond. When the bond reaches maturity, its investor receives its par (or face) value. Zero Coupon Bond - (Definition, Formula, Examples, Calculations) Cube Bank intends to subscribe to a 10-year this Bond having a face value of $1000 per bond. The Yield to Maturity is given as 8%. Accordingly, Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19 Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. Zero-Coupon Bond: Definition, Formula, Example etc. Price of bond = $1,000/ (1+.07)5 = $713.27 Hence, the price that Robi will pay for the bond today is $713.27. Example 2: Semi-annual Compounding Robi is intending to purchase a zero coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 7% compounded semi-annually.

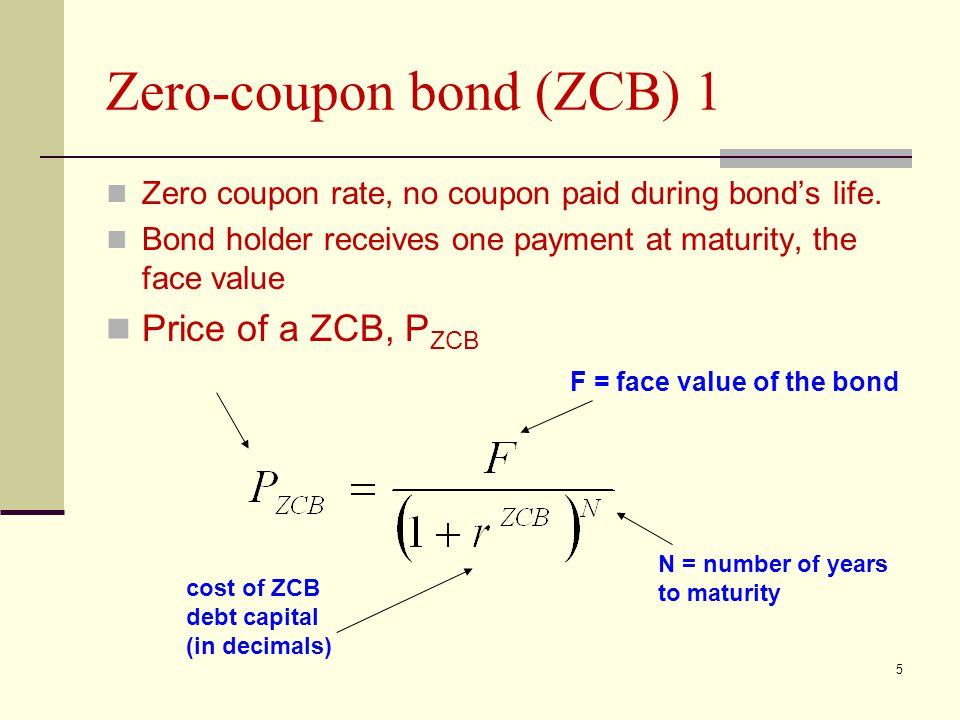

Zero coupon bonds formula. Zero Coupon Bond Yield - Formula (with Calculator) - finance formulas The formula for calculating the effective yield on a discount bond, or zero coupon bond, can be found by rearranging the present value of a zero coupon bond formula: This formula can be written as This formula will then become By subtracting 1 from the both sides, the result would be the formula shown at the top of the page. Return to Top Bond Formula | How to Calculate a Bond | Examples with Excel Template Bond Formula - Example #2. Let us take the example of another bond issue by SDF Inc. that will pay semi-annual coupons. The bonds have a face value of $1,000 and a coupon rate of 6% with maturity tenure of 10 years. Calculate the price of each coupon bond issued by SDF Inc. if the YTM based on current market trends is 4%. Zero Coupon Bond - Explained - The Business Professor, LLC Below is the formula for calculating the present value of a zero coupon bond: Price = M / (1 + r)^n where M = the date of maturity r = Interest Rate n = # of Years until Maturity If an investor wishes to make a 4% return on a bond with $10,000 par value due to mature in 2 years, he will be willing to pay: $10,000 / (1 + 0.04)^2 = $9,245. Risk-Neutral Pricing Formula for Zero-coupon bonds with Default Risk As an example, say a zero is trading at 75, matures at 100 and would recover 25. Then: prob_D * (25-75) + (1 - prob_D) * (100-75) = 0 solves to prob_D = 1/3 You can think of the first half of the above equation, the part prior to the plus sign, as your return (which will be negative) if there is a default prior to maturity.

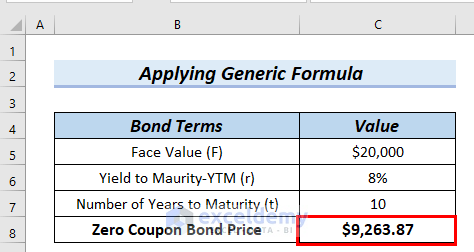

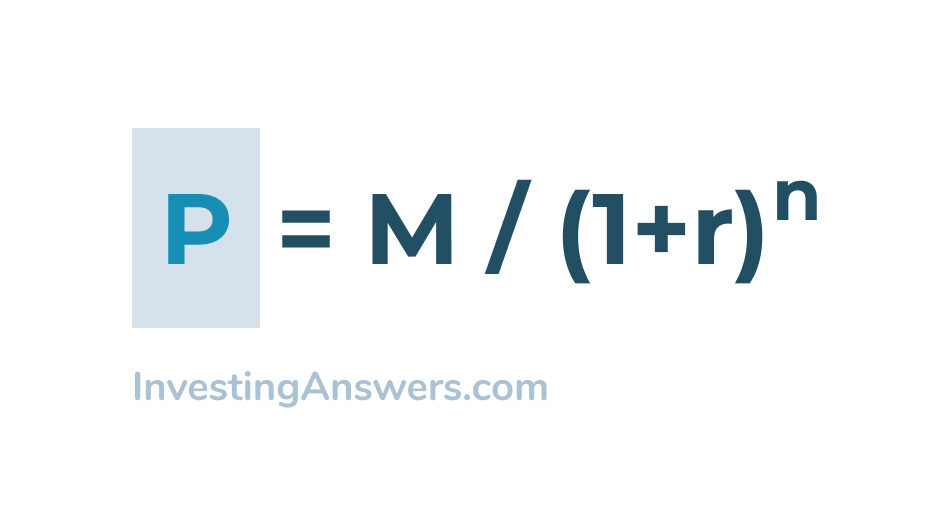

Zero Coupon Bond Default Formulas - QuantWolf Zero Coupon Bond Default Formulas Zero Coupon Bond Default Formula Reference Default probability in terms of price p = 1 − α 1 − R α = P P 0 P = price of the bond P 0 = price of the risk free bond R = recovery rate, between 0 and 1 Default probability in terms of discount rate Zero-Coupon Bond Value | Formula, Example, Analysis, Calculator The formula to calculate the value of a zero-coupon bond is Price = M / (1+r)n where: M = maturity value or face value of the bond r = rate of interest required n = number of years to maturity 3. What is the difference between zero-coupon and traditional coupon bonds? 14.3 Accounting for Zero-Coupon Bonds - Financial Accounting This can be found by table, by formula, or by use of an Excel spreadsheet 1. Because the actual payment is $20,000 and not $1, the present value of the cash flows from this bond (its price) can be found as follows: present value = future cash payment × $0.8900. present value = $20,000 × $0.8900. present value = $17,800. Bootstrapping | How to Construct a Zero Coupon Yield Curve in Excel? Now, for a zero-coupon with a maturity of 6 months, it will receive a single coupon equivalent to the bond yield Bond Yield The bond yield formula evaluates the returns from investment in a given bond. It is calculated as the percentage of the annual coupon payment to the bond price. ... Let us consider a set of zero-coupon bonds of face value ...

Zero-Coupon Bond: Formula and Calculator - Wall Street Prep If the zero-coupon bond compounds semi-annually, the number of years until maturity must be multiplied by two to arrive at the total number of compounding periods (t). Formula Price of Bond (PV) = FV / (1 + r) ^ t Where: PV = Present Value FV = Future Value r = Yield-to-Maturity (YTM) t = Number of Compounding Periods Zero-Coupon Bond - Definition, How It Works, Formula Price of bond = $1,000 / (1+0.05/2) 5*2 = $781.20 The price that John will pay for the bond today is $781.20. Reinvestment Risk and Interest Rate Risk Reinvestment risk is the risk that an investor will be unable to reinvest a bond's cash flows (coupon payments) at a rate equal to the investment's required rate of return. Zero Coupon Bond | Investor.gov Zero coupon bonds are bonds that do not pay interest during the life of the bonds. Instead, investors buy zero coupon bonds at a deep discount from their face value, which is the amount the investor will receive when the bond "matures" or comes due. Zero Coupon Bond Calculator - What is the Market Price? - DQYDJ The zero coupon bond price formula is: \frac{P}{(1+r)^t} where: P: The par or face value of the zero coupon bond; r: The interest rate of the bond; t: The time to maturity of the bond; Zero Coupon Bond Pricing Example. Let's walk through an example zero coupon bond pricing calculation for the default inputs in the tool.

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

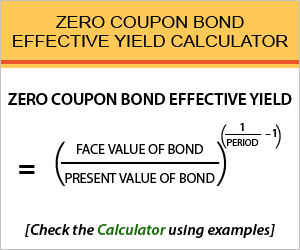

Zero Coupon Bond Calculator 【Yield & Formula】 - Nerd Counter The formula is mentioned below: Zero-Coupon Bond Yield = F 1/n PV - 1 Here; F represents the Face or Par Value PV represents the Present Value n represents the number of periods I feel it necessary to mention an example here that will make it easy to understand how to calculate the yield of a zero-coupon bond.

Bond Formula | How to Calculate a Bond | Examples with Excel ...

Zero-Coupon Bond - Definition, How It Works, Formula Formula for calculating zero-coupon bond yield. Yield is the quantum of returns, usually expressed in percentage, that an investment earns over some time. The yield to maturity (YTM), also called the 'book yield' or 'redemption yield' is the rate of return an investor earns by holding the bond up to its maturity date. Let's illustrate this ...

How to Calculate PV of a Different Bond Type With Excel

How to Buy Zero Coupon Bonds | Finance - Zacks 1. Zero coupon bonds, also known as zeros, are distinct in that they do not make annual interest payments. The bonds are sold at a deep discount, and the principal plus accrued interest is paid at...

Zero Coupon Bonds - Financial Edge

Zero Coupon Bond: Formula & Examples - Study.com Examples of the Zero-Coupon Bond Formula: Example 1: Annual Compounding. Adam wants to invest in a zero-coupon bond with a face value of $1,000 and 9 years to maturity. If the required interest ...

Solved 1 Duration 1. A zero coupon bond with 2.5 years to ...

Zero Coupon Bond Value - Formula (with Calculator) - finance formulas Example of Zero Coupon Bond Formula A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value.

Solved] A 12.75-year maturity zero-coupon bond selling at a ...

Zero-Coupon Bond Definition - Investopedia If the debtor accepts this offer, the bond will be sold to the investor at $20,991 / $25,000 = 84% of the face value. Upon maturity, the investor gains $25,000 - $20,991 = $4,009, which translates...

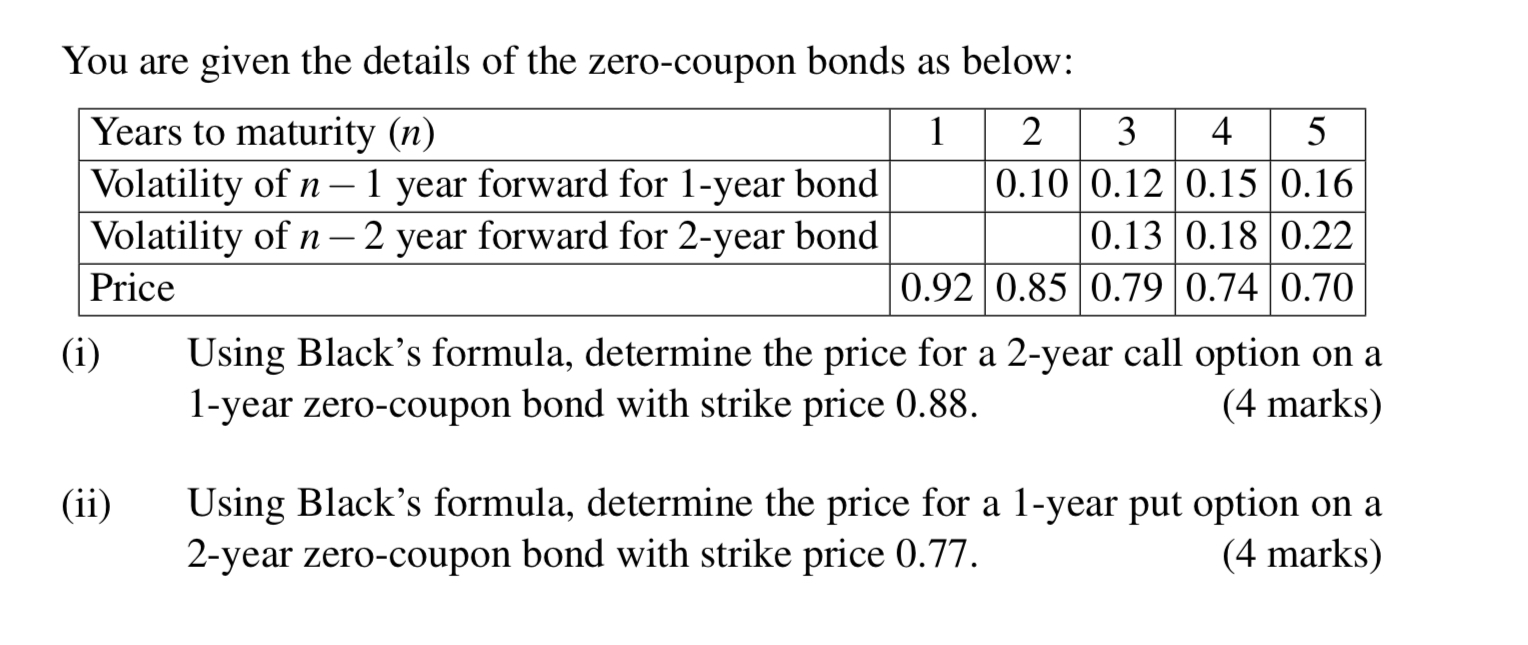

You are given the details of the zero-coupon bonds as | Chegg.com

Zero Coupon Bond Value Formula - Crunch Numbers Price of the zero-coupon bond is calculated much easier than a coupon bond price since there are no coupon payments. It is calculated as: P = \frac {M} { (1 + r)^ {n}} P = (1+r)nM Where P is the current price of a bond, M is the face or nominal value, r is the required rate of interest, n is the number of years until maturity.

hullwhite - Hull white model Monte Carlo simulation Zero ...

Zero Coupon Bond Value Calculator: Calculate Price, Yield to Maturity ... Example Zero-coupon Bond Formula. P = M / (1+r) n. variable definitions: P = price; M = maturity value; ... And it's been a tremendous asset, as a matter of fact, since the early '80s, and we have documented that these zero coupon bonds have outperformed the S&P 500 by five times- that's including dividends in the S&P, but a lot of people, they ...

Impossible Finance — The Perpetual Zero Coupon Bond | by ...

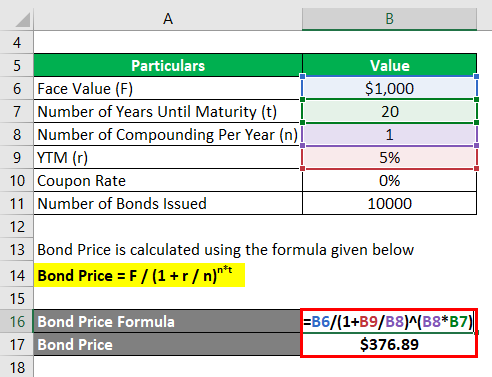

What are Zero-Coupon Bonds? (Definition, Formula, Example, Advantages ... The formula for Zero-Coupon Bonds. The price of zero-coupon bonds is calculated using the formula given below: See also How to Calculate Bond Premium or Discount? (Explained) Price = M / (1 + r) ^ n, where. M = maturity value of the bond. (In other words, the face value of the bond)

SOLVED:Unvolve zero-coupon bonds. A zero-coupon bond is a ...

The One-Minute Guide to Zero Coupon Bonds | FINRA.org Instead of getting interest payments, with a zero you buy the bond at a discount from the face value of the bond, and are paid the face amount when the bond matures. For example, you might pay $3,500 to purchase a 20-year zero-coupon bond with a face value of $10,000. After 20 years, the issuer of the bond pays you $10,000.

Bond valuation

Zero-Coupon Bond: Definition, Formula, Example etc. Price of bond = $1,000/ (1+.07)5 = $713.27 Hence, the price that Robi will pay for the bond today is $713.27. Example 2: Semi-annual Compounding Robi is intending to purchase a zero coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 7% compounded semi-annually.

How to Calculate the Yield of a Zero Coupon Bond Using ...

Zero Coupon Bond - (Definition, Formula, Examples, Calculations) Cube Bank intends to subscribe to a 10-year this Bond having a face value of $1000 per bond. The Yield to Maturity is given as 8%. Accordingly, Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19 Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19.

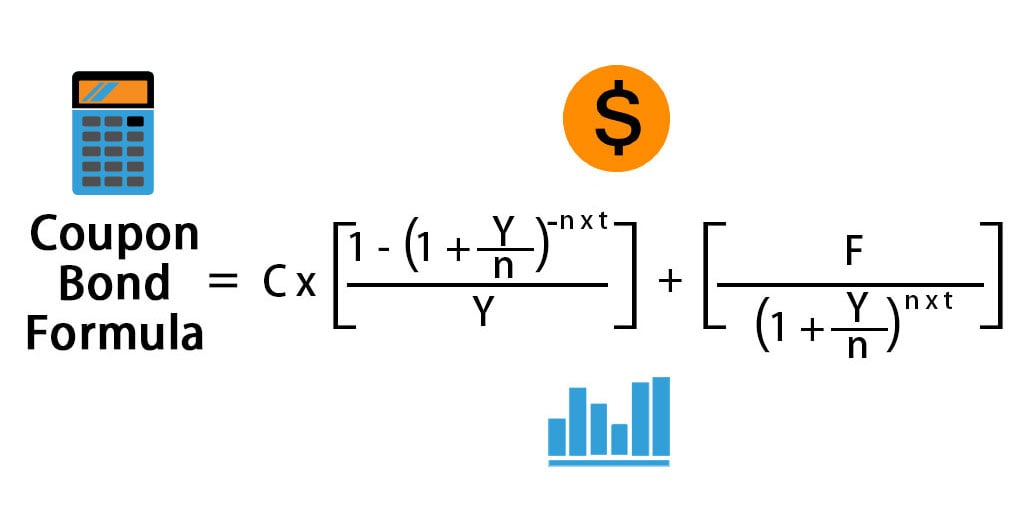

Coupon Bond Formula | Examples with Excel Template

Zero-coupon bond - Wikipedia A zero coupon bond (also discount bond or deep discount bond) is a bond in which the face value is repaid at the time of maturity. [1] Unlike regular bonds, it does not make periodic interest payments or have so-called coupons, hence the term zero-coupon bond. When the bond reaches maturity, its investor receives its par (or face) value.

Zero Coupon Bond Price Calculator Excel (5 Suitable Examples)

Zero Coupon Bond Yield Calculator - Find Formula, Example & more

Zero Coupon Bond Definition and Example | Investing Answers

Price of a defaultable zero coupon bond price in each time t ...

Bond Valuation and Risk - ppt video online download

What is a Zero Coupon Bond? Who Should Invest? | Scripbox

Zero Coupon Bonds Explained (With Examples) - Fervent ...

Yield to Maturity (YTM) Definition & Example | InvestingAnswers

Price of a Zero Coupon Bond using the BAIIPlus

example regarding zero coupon bonds - Quantitative Finance ...

Chapter 6 Bonds 6-1. Chapter Outline 6.1 Bond Terminology 6.2 ...

How to Calculate a Zero Coupon Bond Price | Double Entry ...

Zero Coupon Bond - (Definition, Formula, Examples, Calculations)

Valuing Bonds Bond Cash Flows Prices and Yields

Solved] Complete the information requested for each of the ...

Chapter 5 :BOND PRICES AND INTEREST RATE RISK Mr. Al Mannaei ...

Bond Pricing Formula | How to Calculate Bond Price? | Examples

Zero-Coupon Bond Value | Formula, Example, Analysis, Calculator

Zero Coupon Bond Calculator - Calculator Academy

Zero Coupon Bonds

Calculate the YTM of a Zero Coupon Bond

How to Build a early zero coupon bond amortization table in ...

Graphs of the value of the Defaultable zero coupon bond price ...

Convexity of a Bond | Formula | Duration | Calculation

Zero Bond Discounting Factors - SAP Documentation

I want to know stochastic derivation of zero coupon bond ...

Post a Comment for "39 zero coupon bonds formula"